Tag: digital payments

-

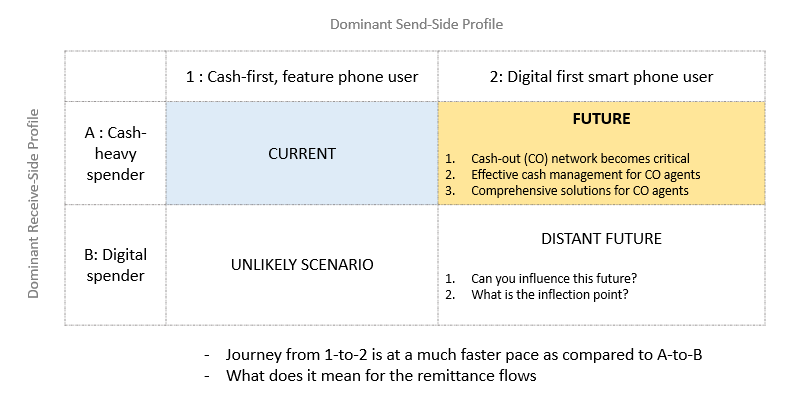

Varying rates of digital adoption across send and receive-sides impact payment-flows

Very simplistically put, payment is the movement of money from A to B. And the world is becoming increasingly comfortable with money flow going digital. Whether its a consumer paying another consumer (P2P) or consumer paying a merchant (P2M) or business paying its vendors/suppliers (B2B) – the levels of digitization of these use-cases is very…

-

A tale of two cards

“Building a visionary company requires one percent vision and 99 percent alignment.” —Jim Collins and Jerry Porras, Built to Last And I believe the alignment needs to show not in meetings but on the ground – in customer interactions, in every process and the decision making across all levels. A recent experience drove home the point very…